Oil to Chemicals

The severe demand destruction due to global lockdowns impacted O2C business. Flexibility in operations and agile response to changing market dynamics enabled operations at near-normal levels and deliver industry-leading results. Domestic demand has recovered sharply across the O2C business.

Highlights FY 2020-21

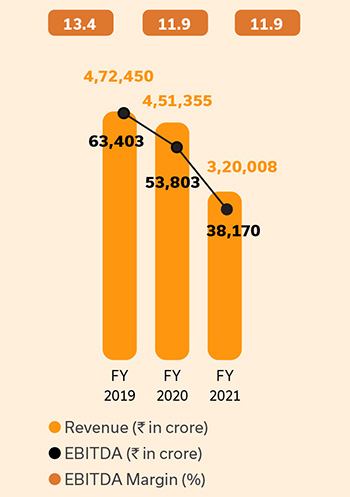

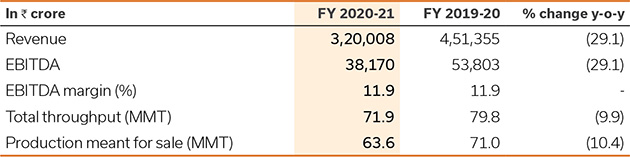

REVENUE  29.1%

29.1%

`3,20,008 crore

EBITDA 29.1%

`38,170 crore

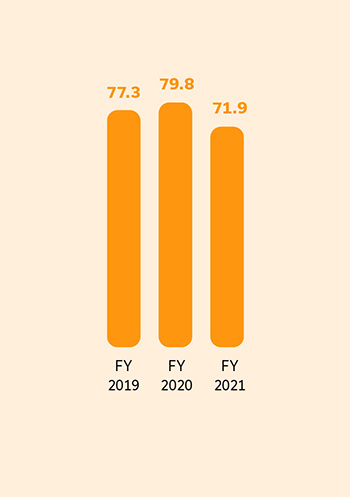

TOTAL THROUGHPUT

71.9 MMT

RIL reorganised its Refinery & Petrochemicals business into Oil to Chemicals (O2C) business in FY 2020-21 to reflect evolving strategy and management matrix. The restructuring is aimed at facilitating faster decision-making while pursuing focused opportunities across the O2C value chain. It will also help attract dedicated pools of capital and create value through strategic partnerships.

The O2C business captures a broad portfolio spanning transportation fuels, polymers, polyesters and elastomers. The deep and unique integration of the O2C business includes worldclass assets comprising ROGC, Aromatics, Gasification, multi-feed and gas crackers along with downstream manufacturing facilities, logistics and supply chain infrastructure.

Specifically, Reliance O2C entity includes refining and petrochemicals plants and manufacturing assets located at Jamnagar, Hazira, Dahej, Nagothane, Vadodara, Patalganga, Silvassa, Barabanki and Hoshiarpur. It also includes 51% equity interest in fuel retailing JV with bp – Reliance BP Mobility Limited (RBML) and 74.9% equity interest in Reliance Sibur Elastomers Private Limited.

1.4 MMBPD

Crude processing capacity

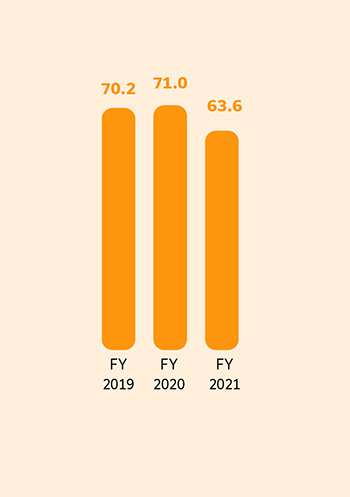

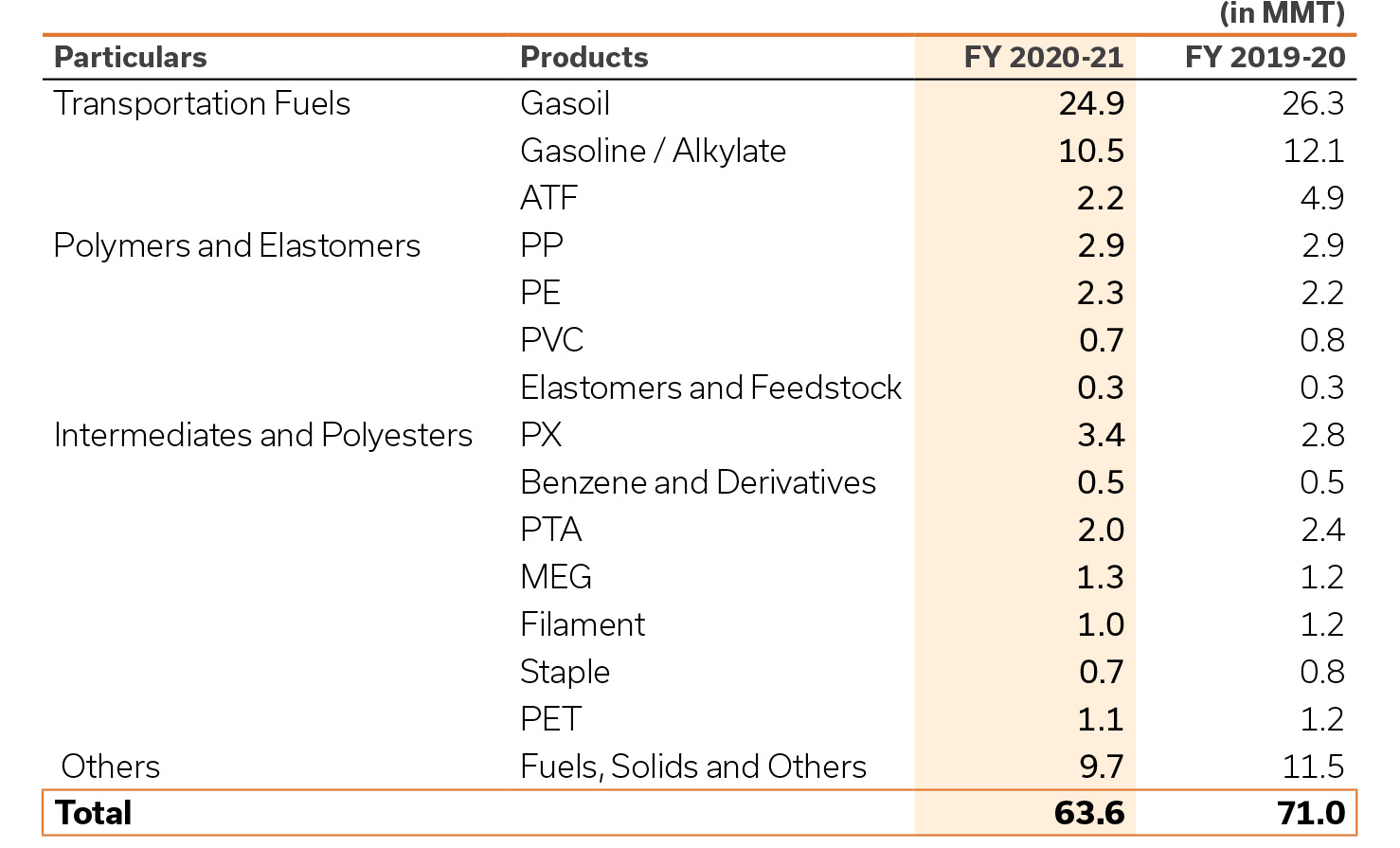

63.6 MMT

Production meant for sale* *FY 2020-21

21.1

Jamnagar site Complexity Index

13

Manufacturing facilities in India (10) and Malaysia (3)

One of the Largest

Integrated polyester players globally

2nd

Largest producer of PX globally

Vision and Mission

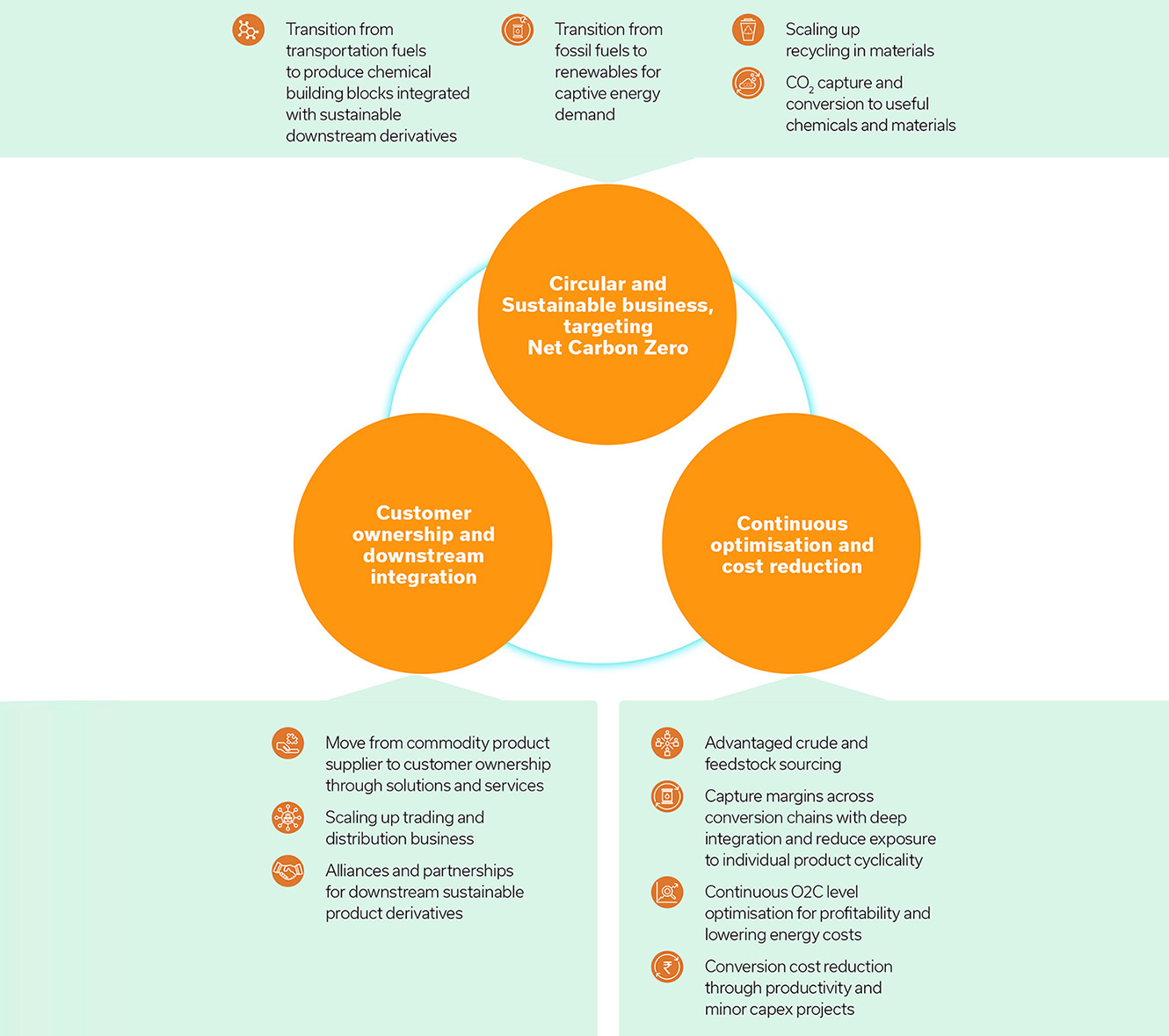

Accelerate new energy and materials businesses while ensuring sustainability through circular economy and target to be Net Carbon Zero by 2035.

Strategic Advantages and Competitive Strengths

Deep and unique integration across sites

- World’s largest and most integrated O2C complex at Jamnagar

- Flexibility to process variety of feedstocks – crude, condensate, naphtha, refinery off-gases, ethane/propane and straight run fuel oil

World-class manufacturing facilities

- Top quartile performance in costs, safety and operations excellence

- One of the lowest cost producers of building blocks – ethylene, propylene and aromatics

Robust portfolio catering to growing consumption markets

- Only company globally, with integration from oil to polymers, chemicals, polyesters and elastomers

- Allows margin capture across industry value chains and reduces exposure to cyclicality

Unparalleled logistics and supply chain network

- 5x bigger distribution footprint than nearest competitor in India; unique pan-India reach leveraging multi-modal logistics

- Serving 11,000+ customers for chemicals and materials across India through 16 regional offices and 61 warehouses

- Serving transportation fuels to retail customers everyday at over 1,400 outlets

Performance Summary

REVENUE AND EBITDA

TOTAL THROUGHPUT (MMT)

PRODUCTION MEANT FOR SALE (MMT)

Operating Framework

The key priorities of the O2C business are as under

Highlights FY 2020-21

Delivered resilient performance despite unprecedented challenges and macro headwinds

Operated plants at near-full capacity while ensuring the safety of employees and communities, even as global and domestic peers substantially lowered operating rates and even shut down plants completely during 1Q FY 2021

Agile business model (domestic to export and back to domestic as per market demand) leveraging our global customer base and multimodal distribution capabilities

Ramped up the capacities to produce 1,00,000 personal protective equipment (PPE) per day during the peak of pandemic

Reliance and bp commenced operations of their new Indian fuels and mobility joint venture - operating under the ‘Jio-bp’ brand – which aims to become a leading player in India’s fuels and mobility market

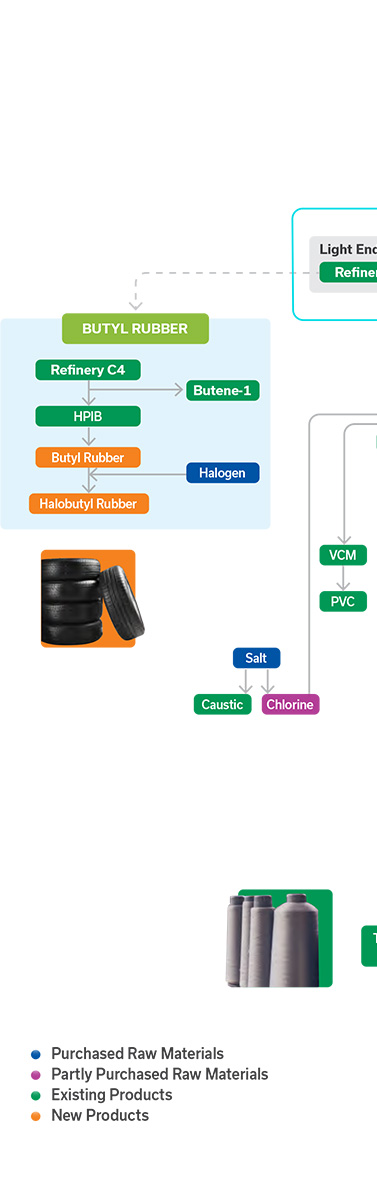

Successfully commissioned the Halobutyl-Rubber Plant in partnership with SIBUR

Developed in-house Reliance Olefin Removal Catalytic (REL-ORCAT) Technology

SEZ refinery won the prestigious ‘Refinery of the Year’ award from Federation of Indian Petroleum Industry (FIPI)

Petrochemicals business won ‘Company of the Year’ award from FICCI for our significant value creation in society and contributions towards fight against COVID-19

Industry Overview

FY 2020-21 was characterised by unprecedented volatility in crude oil and feedstock prices. It was a year of two halves – significant demand contraction in the first half due to pandemic-related lockdowns followed by a sharp recovery in economic activity and demand revival with fiscal stimulus in the second half.

Crude Oil Demand and Supply

Global oil demand plunged by 16.2% y-o-y in 2Q CY 2020 to 82.9 mb/d. It recovered sharply to 92.6 mb/d in 3Q CY 2020. Overall demand in CY 2020 was at 91.0 mb/d, 8.7% below that in CY 2019. China was the only country to register growth.

OPEC and several other oil exporting countries carried out coordinated supply cuts, which peaked at 9.7 mb/d during May-June 20 and averaged 5.3 mb/d for CY 2020. These cuts helped reduce crude inventories and rebalance supply and demand supporting oil prices.

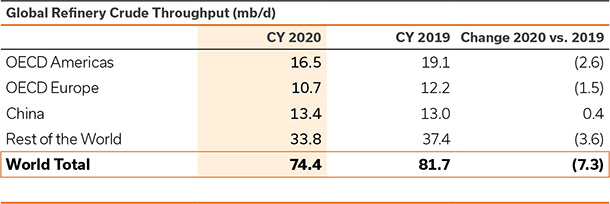

Global Refining Operations

Source: IEA

In CY 2020, refining runs were lower by 7.3 mb/d from a year earlier, while demand declined by 8.7 mb/d. This resulted in weaker margins and permanent closure of refineries. Globally, announcements have already been made for the permanent closure of ~3.4 mb/d refining capacity by 2023.

OIL PRICES

(US$/bbl)

Source: IEA

Crude Oil and LNG Prices

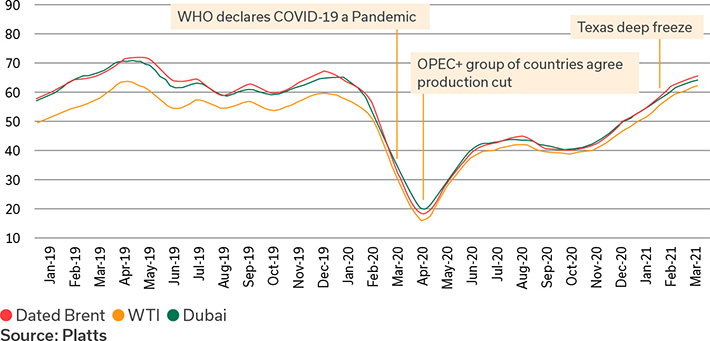

Crude prices plummeted during 1Q FY 2021 with Brent crude oil touching a low of US$18.5/bbl in April 2020. However, the sharp supply cuts, coupled with disruptions in February 2021 due to Texas freeze, pushed crude prices back to pre-pandemic levels in March 2021

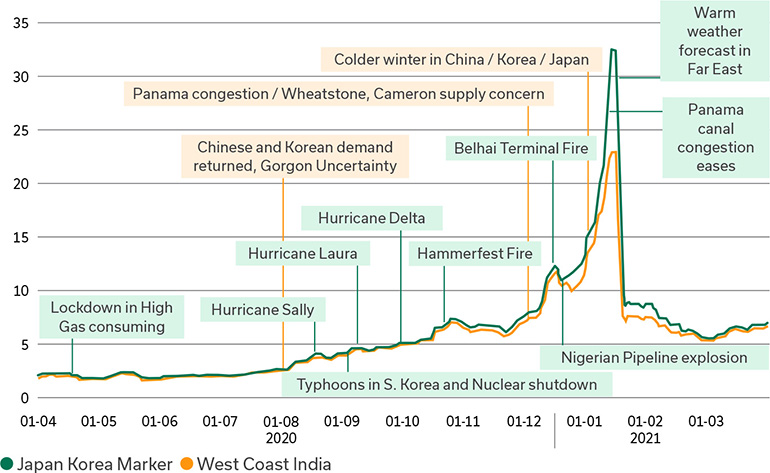

LNG prices were highly volatile during the year, with prices in Asia starting at a low level of around US$2/mmbtu at the beginning of the year due to demand drop before peaking at US$32.50/ mmbtu in January 2021 due to supply disruptions in Nigeria, Panama Canal congestion and colder winter in Far East. Prices have since then cooled with the restoration of supplies.

Cost of shipping crude surged in March 2020 and continued to be high in April 2020 as weak demand for prompt supplies had seen an increasing number of tankers booked for floating storage. In clean freight markets, demand for floating storage caused shipping rates to soar in April 2020. From May 2020, freight rates normalised for both crude as well as products as global crude production fell sharply and reduced interest in floating storage with lower production.

LNG PRICE ASSESSMENT

(US$/mmbtu)

Transportation Fuels

Global Market Environment

Global gasoline and gasoil demand in

CY 2020 was lower by 3.0 mb/d and

1.8 mb/d respectively compared to

CY 2019. Gasoline demand recovered

quickly from the lows in 2Q CY 2020, as

preference for use of personal vehicles

for daily commute increased during

the pandemic. Diesel demand was also

adversely impacted, before recovering

in-line with revival in economic activity.

Jet fuel demand was the worst hit due to

stringent restrictions on air travel, falling

40.6% from the previous year.

Domestic Market Environment

India’s petroleum products demand

contracted by 9.1% to 195 MMT in

FY 2020-21; LPG demand maintained

an upward growth trajectory. India’s

demand for gasoline and gasoil

rebounded sharply in the second

half, but overall demand in FY 2020-

21 was still down by 6.7% and 12%,

respectively. Gasoline sales returned to

pre-pandemic levels in September 2020.

The aviation industry was the worst hit.

Domestic flights resumed in a calibrated manner from May 2020 and reached

70% of pre-pandemic levels by the end

of FY 2020-21. Jet/Kero demand fell

sharply by 47% y-o-y.

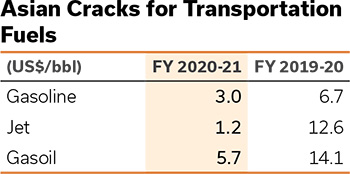

Margins

During FY 2020-21, 10 ppm gasoil and Jet/Kero cracks in the Singapore market were down by 60% and 90% y-o-y respectively. Low jet fuel demand due to disruption in air travel and tourism industry made refiners shift yield towards the gasoil pool, capping gasoil cracks upside.

Gasoline 92R cracks were lower by 55.3% y-o-y, as lockdowns resulted in reduced mobility across the globe. High spare capacity and inventory levels weighed on gasoline cracks.

However, in 1Q CY 2021, gasoline cracks touched pre-pandemic levels while gasoil and jet cracks continued to lag at 49% and 39%, respectively.

Source: Platts

Global Cracker Operations

Global demand for ethylene registered a moderate 1.7% y-o-y growth to 166 MMT in CY 2020 from 163 MMT in CY 2019, while operating rates fell to 86% from 90%. New capacity addition of 11 MMTA during the year significantly outpaced demand growth. The liquidity crunch caused by the pandemic delayed start-ups as well as final investment decisions for new projects.

Ethane and Naphtha Prices

Average naphtha prices in Asia were down by 21% y-o-y in FY 2020-21 amidst softening of crude price in 1H FY 2021 and slowdown of demand due to low global economic activity. However, prices recovered in 2H FY 2021 with healthy demand from downstream chemicals/ products, improving demand of gasoline blending and higher crude prices.

Polymers and Elastomers

Global Market Environment

Demand destruction in certain sectors

like automotive, housing and construction

and white goods/consumer durables had

a negative impact on the downstream

business. At the same time, the pandemic

resulted in surge in demand for polymers

and polyesters from the health & hygiene,

packaging and e-commerce sectors.

Global polymer demand [for polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC)] in CY 2020 was 230 MMT, up by 2% y-o-y. Global PP and PE demand grew by 3% in CY 2020, led by Asia, especially China and India. Demand for PVC remained subdued during the year as a sustained high price environment caused shift to alternative products. Global demand for Polybutadiene Rubber (PBR) and Styrene-Butadiene Rubber (SBR) elastomers contracted by 6% and 7% respectively during CY 2020, on the back of weak automotive sector demand.

Domestic Market Environment

PP demand in the country grew at

a marginal 2% y-o-y on account of

subdued demand from the auto sector

and overall lower consumption owing to

the pandemic in 1H FY 2021. However,

demand from the health & hygiene

sector, raffia and Biaxially Oriented

Polypropylene (BOPP) packaging

remained buoyant. PE demand registered

a healthy growth of 7% y-o-y, driven

by e-commerce, FMCG and liquid

packaging. Policy boost for several

water and sewage pipeline projects

further pushed polymer demand.

The all-time-high prices of PVC caused

a slight demand shift to alternative

materials for the pipes sector.

Elastomer demand gradually recovered as the operating rate of the auto majors increased gradually from 25% in May to 80% in July, and supply chain hurdles eased with the lifting of the lockdown. Tyre majors registered a good performance in 2H FY 2021 amid strong farm and 2/3-wheeler tyre demand which drove up domestic demand for SBR to 7% y-o-y, while PBR demand remained flat.

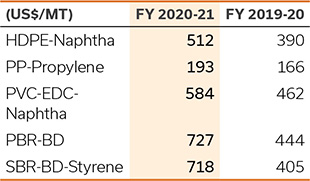

Margin

Polymer prices weakened at the

beginning of 2020, but gradually

improved by the second quarter on

the back of healthy demand from

the essential goods and services

sector. Global operating rate for

PP and PE averaged 86% and 85%

respectively during 2020. Polymer

margins strengthened especially in

2H FY 2021 with recovery in demand,

reduced availability due to supply

chain constraints and polar freeze in

USGC. Integrated PP-Naphtha and

HDPE-Naphtha margins expanded 22%

and 31%, respectively. PVC margins

were at multi-year high amidst supply

shortages. Elastomer margins remained

strong, especially towards the end

of the year, due to lower feedstock

prices and supply constraints. Margins

trended above 5-year average and were

up 64% and 77% y-o-y for PBR and

SBR, respectively.

Southeast Asia Polymer Margins

Source: Platts and ICIS

Intermediates and Polyesters

Global Market Environment

Global demand for Intermediates

(MEG/PX/PTA) fell by 6% to 143 MMT

in CY 2020 from 152 MMT in 2019.

PX markets improved in the latter part

of the year due to new downstream

PTA capacity additions. PTA markets

remained healthy as downstream operating rates went up despite rising

inventory in the first half of the year.

MEG demand strengthened in the latter

part of the year due to supply concerns

from the US, and this was reflected in

declining port inventories.

Overall demand for polyesters was marginally lower by 6% to 77 MMT. The pandemic adversely affected the global demand for textiles and apparels, but demand for PET (face shield), LAB (detergent products) and non-woven staple fibre (PPE kits, face masks, and polyester swabs) witnessed a surge.

Domestic Market Environment

Domestic demand for intermediates

was impacted due to demand

destruction in the textile and polyester

industry at the time of the pandemic.

Demand for the year contracted by

~14%, reflecting pandemic’s impact on

downstream sectors.

The downstream polyester industry in the country bore the brunt of the nationwide lockdown and the closure of downstream units due to mass labour exodus. The industry revived with the gradual easing of the lockdown and festive season demand, reaching pre-pandemic levels by the end of FY 2020-21.

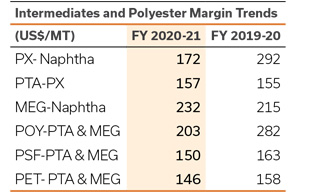

Margins

With reduced global gasoline blending

demand, integrated chemical

complexes continued to ramp up PX

production. This resulted in a high PX

inventory (up to 4 MMTA) in China,

which was further impacted by capacity

expansions of 1.8 MMTA. Global PX

operating rates dropped to 71% in 2020

on the back of unprecedented capacity

expansions in China. PX prices dropped 28% while PX-Naphtha margins

dipped 41% y-o-y, well below 5-year

average levels.

PTA markets in China remained oversupplied given the capacity addition of 9.9 MMTA and large market inventories. Global PTA operating rates dipped to 78% in 2020. Overall, in FY 2020-21, PTA prices dropped by 21% while PTA-PX margins firmed up by 1% y-o-y.

Global MEG markets witnessed capacity addition of ~3.7 MMTA in an already over supplied market. Global MEG operating rates dropped to 66%. However, in the second half of FY 2020-21, MEG markets strengthened as supplies from the US were impacted by hurricanes and the Arctic freeze. High polyester operating rates also kept sentiments healthy. MEG prices dropped by 9% and MEG-Naphtha margins firmed up by 8% y-o-y.

PET markets witnessed a slowdown as consumption of beverages witnessed a dip amid the global pandemic. However, demand in the health sector and packaging improved. PET prices dropped by 16% and margins dipped by 8% y-o-y.

Source: Platts, ICIS, CCFGroup

Performance Update

Financial and Business Performance

Financial Performance

11.9 %

EBITDA margin

71.9 MMT

Total throughput

The O2C business experienced both price and margin dislocation due to the pandemic and lockdown in many countries in 1H FY 2021. Even in testing times such as this, the business delivered robust performance by leveraging the strong international and domestic supply chain, multimodal logistics, deep integration and feedstock flexibility.

Revenues for the O2C business declined 29% with lower volumes and lower realisation due to decline in average crude and feedstock prices. Brent crude price for the year averaged at US$44.3/bbl versus US$61.1/bbl in the previous year.

EBITDA was also lower with weak demand environment across products in 1H FY 2021. The segment performance was supported by a sharp recovery in downstream demand and deltas in 2H FY 2021.

Business Performance

Production Meant for Sale

Overall production meant for sale reduced from 71 MMT to 63.6 MMT. Most of the reduction came from transportation fuels due to global demand destruction. However, with an agile business model and the ability to optimise feedstock usage, Reliance was able to run downstream plants at full throughput.

Transportation Fuels

The strong network presence on the highways and industry-leading fleet programme (Transconnect) helped recover gasoline and gasoil volumes to pre-pandemic levels. Strong Quality and Quantity (Q&Q) assurance also contributed to the volume recovery.

In FY 2020-21, bulk diesel industry volumes shrunk by 22% on y-o-y basis. Despite facing a contraction of 17% y-o-y, RIL did better than the industry and increased its market share to 9.3%, focusing on the infrastructure, construction and mining segments.

Reliance BP Mobility Limited (RBML), a 51:49 joint venture of Reliance Industries Limited (RIL) and bp, went live on July 10, 2020. RBML operates under the ‘Jio-bp’ brand.

RBML, with its network of 1,419 outlets and fleet programme (Transconnect), fully recovered its pre-pandemic gasoline and gasoil sales volumes.

RBML, with its network of 1,419 outlets and fleet programme (Transconnect), fully recovered its pre-pandemic gasoline and gasoil sales volumes.

1,419 outlets

In the RBML network

5,500 outlets

Proposed network post expansion

RBML has become India’s largest fuel door delivery network for specified use, with presence at 1,083 sites in 21 states. RBML has launched light-weight and tamper-proof high density PE fuel containers for doorstep delivery which promises operational ease, efficiency, and quantity and quality (Q&Q) assurance.

In August 2020, RBML took over the operations of RIL aviation fuel stations across the country. It aspires to bring industry-leading technology, best-in-class service and innovative customer-centric solutions to aviation fuelling. RBML fuelled medical, repatriation and cargo flights across India at the peak of the lockdown.

Reflecting the Net Carbon Zero target of RIL, RBML aspires to provide Indian consumers with advanced fuels that have lower emissions, charging infrastructure for electric vehicles and other low carbon solutions.

To support the proposed network expansion of up to 5,500 outlets over five years, RBML kickstarted its franchise onboarding process. It has initiated infrastructure development at all supply locations and started pilot testing of battery swap stations at over 24 select locations. Initial response has been encouraging with strong growth in daily order deliveries.

RBML is committed to create a world class fuelling experience for its customers, with proven customer value proposition, synergies of extended group companies (RIL and bp), company-wide focus on customer centricity and best-in-class technology.

Polymers and Elastomers

RIL maintained steady polymer production with reliable operations across sites and achieved the highest ever PE production in FY 2020-21. It maintained operating rates higher than its peers due to its keen focus on exports in the first half, and its ability to ride on a buoyant market in the second half. RIL maintained its market leadership in polymers, with a domestic market share of 34%. It exported 1.3 MMT of polymers across the world during the year.

RIL’s agile supply chain helped place 80% polymer products in the export market within 10 days during the challenging 1Q FY 2021, as against 20% during the pre-COVID period. This helped in operating plants at near full capacity of 98% during 1Q FY 2021 while the rest of the domestic industry operated at 60% levels.

Intermediates and Polyesters

A total of 2.1 MMT was exported in FY 2020-21 across the entire polyester chain. RIL also maintained its market share in the domestic polyester market. Significant PX and Benzene exports in 1H FY 2021 helped maintain the operating rate of aromatics plants. PTA exports during 1H FY 2021 were impacted, curtailing PTA production. Demand destruction in MEG was countered by diverting the surplus volume into exports market.

RIL continued to explore new products and market segments with the introduction of biodegradable polyester and R3S in the paint segment. At the same time, given the unique circumstances, RIL focused on developing essential products like PPE suits, polyester swabs and other medical applications to cater to the needs of critical segments like health and hygiene.

Leadership in adopting circular economy in India

RIL is committed to supporting and leading the industry on circular economy and sustainability. The Company constantly endeavours to imbibe the concept of circularity in its operations and processes. Cognisant of the fact that achieving this objective requires long-term commitment and collaboration amongst various stakeholders, it supports like-minded organisations, NGOs and individuals in waste recycling and diverting post-consumer waste away from landfill while creating awareness about the environment among consumers.

RIL has identified short, medium and long term strategies to support a circular economy for plastics. In the short term, the focus is on increasing the Company’s PET recycling footprint and usage of Multi-layered Plastics (MLP) for road construction. In the medium term, it is focusing on polyolefin recycling and ‘waste to oil’ strategy. In the long term, the Company is looking at chemical recycling, plastic waste composites and design for circularity. Various initiatives are on the go.

R|ELAN™ — Circular Design Challenge

During FY 2020-21, R|Elan™ initiated the third season of

Circular Design Challenge (CDC) in partnership with the

United Nations Environment Programme (UNEP) at the

Lakme Fashion Week (LFW) in March 2021. In partnership

with IMG and UNEP, R|Elan™ unveiled the collection ‘Malai’,

winner from the second edition of LFW. The collection uses a

bio-composite material made from the agricultural waste of

South India’s coconut industry. With circularity at the core

of all six designers’ portfolio, CDC 3.0 showcased stunning

collections made from materials like discarded tarpaulin,

post-consumer clothing, handwoven and upcycled textiles,

waste denim and recycled PET bottles.

Collaboration with Pankaj and Nidhi at LFW

R|Elan™ has been consistently supporting circularity in the

fashion industry. During the year, the brand collaborated with

the famous designer duo, Pankaj and Nidhi, for the second

time to showcase its latest collection at the first-ever digital

edition of LFW.

The new collection showcased R|Elan™ GreenGold, made from 100% recycled PET bottles, R|Elan™ FeelFresh, which has anti-microbial properties, and R|Elan™ Kooltex, which keeps the wearer cool and comfortable for a longer time.

Launch of waste reduction programme

R|Elan™ collaborated with Forest Essentials™, the Ayurvedabased

skincare and perfume brand, in September 2020 to

encourage recycling of used plastic packaging. As part of the

collaboration, Forest Essentials™ created a collection facility

in each of its major stores across the country. Customers are

being encouraged to drop empty jars and bottles into these

facilities through a reward programme. The waste collection is

to be processed and repurposed to make GreenGold™ fibres

and fabrics for apparel, bags and other applications.

Anti-microbial mask from R|Elan™

#FeelSafeFeelFresh Campaign

R|Elan™ tied up with India’s leading brand, Proline® to create

a range of attractive, high performance masks using R|Elan™

FeelFresh™ fabric with anti-microbial attributes. The Proline®

Reusable Protection Mask has a three-layer triple particle

filtration system and offers the superior fabric qualities

of R|Elan™ FeelFresh™, which is embedded with silver

technology to provide long lasting protection

Alliance to end plastic waste

RIL is the founding member and the lone Indian company to

participate in the global effort to eliminate plastic waste in

the environment through the Alliance to End Plastic Waste

(AEPW). The Company aims to bring the best technologies

and companies to India for elimination of plastic waste.

Support for Indian Centre for Plastics in the

Environment (ICPE)

RIL continues to support ICPE communication initiatives

by supporting the ‘Fight Pollution, Not Plastics’ (FPNP)

awareness campaign, school engagement campaigns and

an all-India creative competition to find ways to reduce

plastics pollution.

Reverse vending machine

RIL has sponsored more than 100 reverse vending machine

installations across major cities to enhance awareness

amongst the public about plastic waste

Scaling up Digital Platforms to Enrich Customer Experience

The COVID-19 pandemic led to a sudden change in the way of working, supported and sustained by digital collaboration platforms. The following digital initiatives were implemented in a short span of time to support the shift in business condition and ensure seamless migration to a virtual working environment.

Digital customer experience

- Collaborative planning through CRM platform to effectively manage customer demand

- Mobility apps for approvals, account management and customer visits to empower the sales team for better customer service

- Secured document sharing platform (E-Room) for effective (finance, shipping and forwarding documents) collaboration with internal as well as external bodies primarily with a work-from-home focus

Digitalisation in supply chain, planning and optimisation

- Warehouse Management (EWM) operated mobility solutions on smart devices, which simplified complex logistics, optimised inventory tracking, distribution operations and multi-channel fulfilment

- Improved profitability through digitalisation of the integrated value chain planning and optimisation for all downstream products, including Recron Malaysia and integration with upstream at Cracker

Digitisation and Analytics for process optimisation

- SCM Spend Analytics to include components like shipping, multimodal and chartering (bulkers)

- Export General Manifest (EGM) downloads from ICEGATE (e-commerce portal for central excise and customs) are now automated through deployment of bots

- Export documentation processes like LC Scrutiny, SI (Shipping Instruction) BL (Bill of Lading) scrutiny and SI filing with shipping line portal are digitised and automated with the help of AI/ML

- Trip check application was rolled out on tab devices at downstream secondary warehouses. Major components of this application are Truck Health Check, Trip Check (Pre- Load) and Trick Check (Post-Load)

CASE STUDIES

Ecosystem for indigenous PPE production

RIL scaled up production of PP fibre and filament grades that are used as raw material for N95 masks and PPE suits. It developed very high-flow melt blown grades (1800-2300 MFI) in collaboration with a domestic compounder and masterbatch manufacturer to produce indigenous PPE kits with higher Particulate Filtration Efficiency (PFE). As a result, India became the world’s 2nd largest PPE kit manufacturer and net exporter, even though it did not have capacity to produce PPE kits till January 2020.

1 lakh/day

Production of PPE kits and N95 masks

Redefining fuel retailing through e-commerce in India

RBML is the first Oil Marketing Company (OMC) to get the approval of Mobile Dispensing Unit and the only OMC to use HDPE containers (non-metallic) for on demand delivery of fuel. With its services spanning across India, it is uncovering the latent needs of the non-transport sector, and meeting these needs with great efficiency, leading the way to market leadership in the non-transport sector.

Transconnect: Building strong relationships

RBML’s large network, channel participation and field force focus with customised IT tool helps it drive volume. The Transconnect programme helps it ease the transaction process through secure card-less solution (Trans-mobile). Through Transconnect, RBML leveraged contactless operational capability during the lockdown, leading to significantly higher fleet volume share and highest ever monthly sales in FY 2020-21.

Outlook

Global vaccination drive and large stimulus programmes will influence consumer sentiments and demand growth, in the medium term. Oil demand is expected to recover in CY 2021 to 96.4 mb/d, still below CY 2019 levels of 99.7 mb/d as per IEA. However, tightness in the crude oil market and strong prices are likely to continue due to OPEC+ cooperation.

Global transportation fuels demand (except Jet fuel) is likely to reach pre-COVID levels only by the end of FY 2021-22. Container shortages are expected to continue through 1H FY 2022, supporting margins for polymers and intermediates.

Strong domestic demand across key segments such as healthcare, packaging, durables, auto and infrastructure is expected to drive demand for downstream products. Near term demand trends can be impacted by the ongoing second wave of the pandemic and fresh restrictions.